In commercial real estate, numbers tell the story, and as the third quarter of 2024 unfolds, the figures are beginning to shift the perception of future deal flow toward cautious optimism.

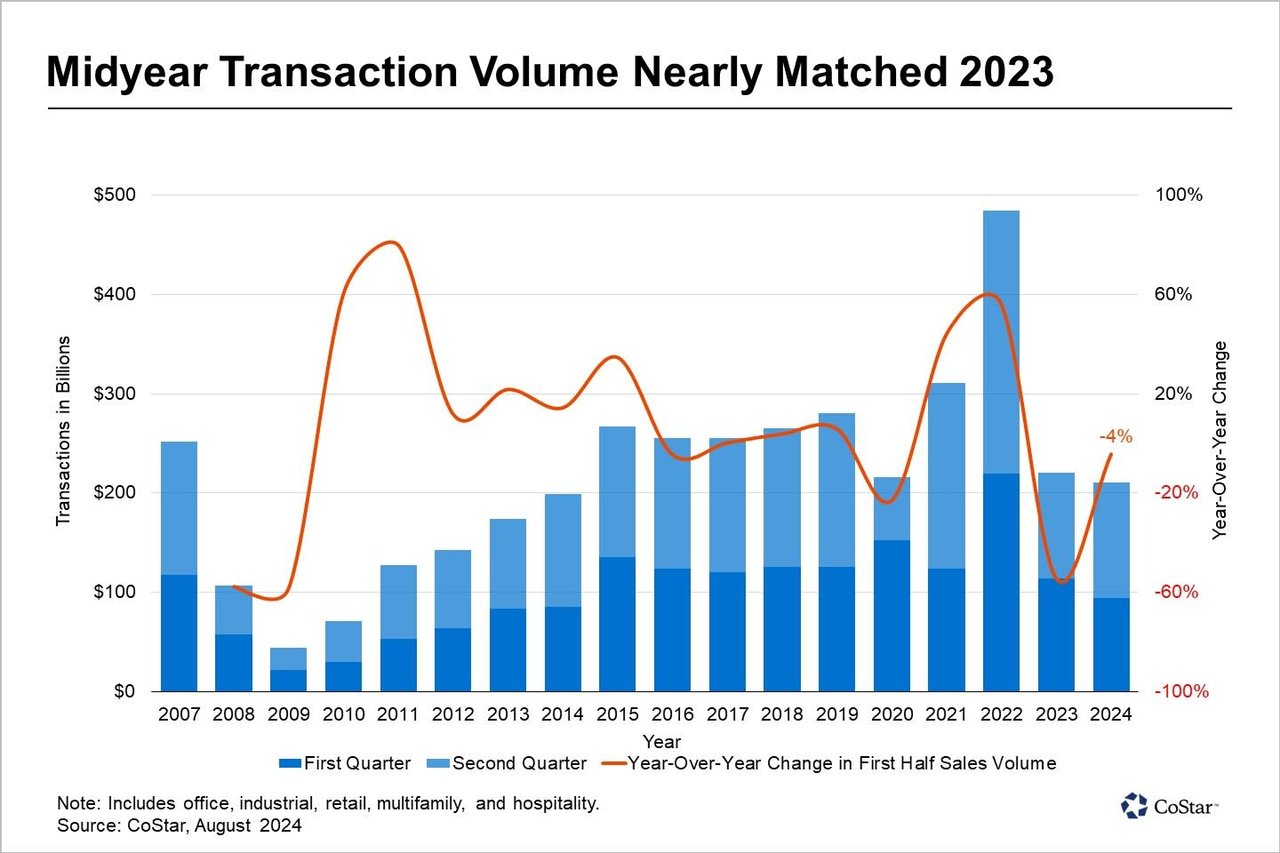

Through June of this year, total property sales of $211 billion exchanged hands across the five key sectors — office, industrial, retail, multifamily and hospitality. And while this represents a 4% decline from the previous year, overall transaction activity shows early signs of regaining its footing.

The turbulence of 2023, driven by soaring interest rates in the third quarter and deepening recession fears in the fourth, cast a long shadow over the market. Many sellers, wary of the economic uncertainty, hesitated to test the waters, holding back assets that might have otherwise hit the market.

As a result, transaction volume remained flat and bypassing its usual year-end surge. But as 2024 progresses, the tide seems to be turning.

The first quarter of 2024, still reeling from the previous year’s challenges, saw just $94 billion in deals — a 17% drop from the same time in 2023. Yet, the second quarter brought a renewed sense of optimism, with $117 billion in property changing hands, marking a 9% increase from the year before.

This cautious optimism extends beyond the recent uptick in sales. The market now watches closely for a potential interest rate cut by the Federal Reserve in September, a move that could align perfectly with the fall selling season.

As new investment opportunities flood the market after Labor Day, the prospect of lower borrowing costs could be the spark needed to accelerate deal flow. Armed with the potential for more favorable debt, buyers might find the confidence they’ve been waiting for, setting the stage for a robust finish to the year.

Taking a broader perspective and comparing current sales figures to pre-pandemic five-year averages reveals a clearer momentum. The first quarter of 2024 reached just 75% of the five-year average for the previous first quarters, but by the second quarter, that figure had climbed to 84%. This upward trajectory suggests the market is regaining its previous rhythm, with each quarter building toward a crescendo in the fourth quarter.

Meanwhile, core property markets such as New York, Los Angeles, Dallas-Fort Worth, Atlanta, Chicago and Boston are already outpacing their prior two-year averages for property sales, signaling that transaction volumes may have found a bottom. In other major markets, such as Denver, Miami, Minneapolis, Orange County, San Diego and San Jose, transaction volumes hover around their two-year averages, indicating a stabilization that could herald a broader market recovery.

As 2024 enters its final stretch, the focus remains on the Federal Reserve and the potential for interest rate cuts. Should the current trend hold, with third-quarter volumes surpassing those of the second, the market could be on the brink of resurgence. The recent slump in transaction volumes could soon be a thing of the past as the commercial real estate sector regains momentum in deal flow, even as uncertainty around pricing persists.